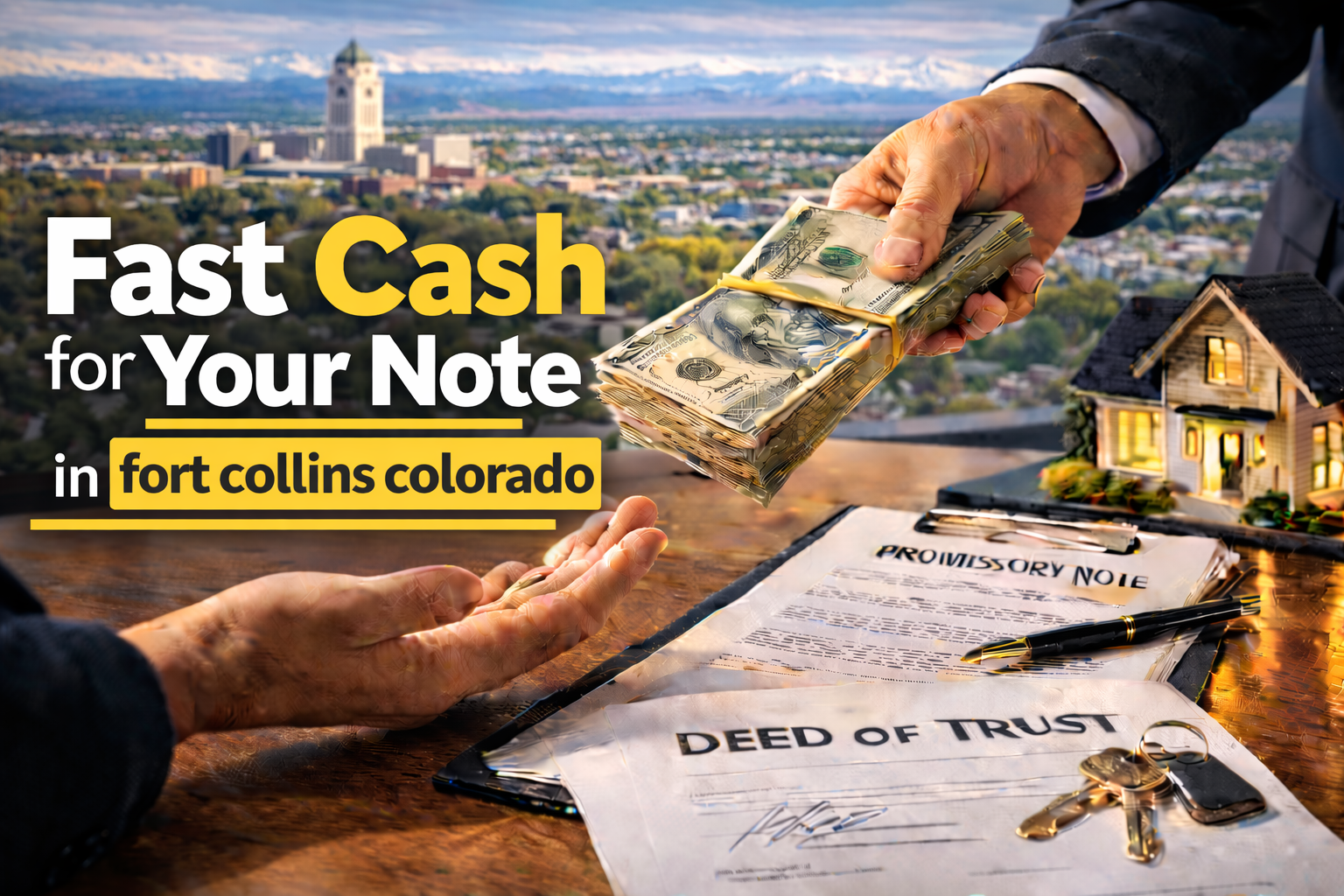

If you’re looking to sell your mortgage notes fast in Fort Collins, CO, you need a process that’s straightforward, reliable, and built for speed. Whether you hold a performing or non-performing note—residential or commercial—Trusted Note Buyer offers a direct, no-nonsense solution. The Fort Collins real estate market is known for its steady growth and strong demand, but selling a note through traditional channels can be slow and unpredictable. We eliminate the waiting, the uncertainty, and the hassle by buying your note directly, with no brokers and no hidden fees.

Here’s how it works: Start by submitting basic information about your note using our secure online form. We review your details and respond quickly—often within 24 hours—with a transparent, competitive cash offer. There’s no obligation and no pressure. If you accept, we handle all the paperwork and coordinate with local title companies to ensure a smooth, compliant transaction. You get paid fast, typically within days, not weeks or months. Our process is designed for your convenience and peace of mind, so you can move on from your note without delays or surprises.

What sets us apart is our commitment to honest, upfront pricing and a seamless experience. Unlike brokers who shop your note around and take a cut, we buy directly, which means you keep more of your money and avoid unnecessary complications. We understand the unique dynamics of the Fort Collins market, from its vibrant downtown to its expanding residential neighborhoods, and we tailor our offers to reflect current property values and local demand. Our team brings years of experience and a reputation for integrity, so you can trust that you’re getting a fair deal.

If you’re ready to sell your Fort Collins, CO note fast for cash, Trusted Note Buyer is here to help. Experience a fast, easy process with no middlemen, no surprises, and no delays—just a straightforward sale and quick payment. Get started today and see how simple selling your mortgage note in Fort Collins can be.

Foreclosure Notes in Fort Collins

Foreclosure notes are a type of real estate note secured by properties where the borrower has defaulted on their mortgage payments, resulting in the lender initiating foreclosure proceedings. These notes represent the right to collect the outstanding debt and, potentially, to acquire the underlying property if the foreclosure process is completed. The legal pathway for foreclosing on a property varies by state; in Colorado, the process may be court-based (judicial) or handled by a trustee (non-judicial), and the applicable method can impact both the duration and complexity of the proceedings. It is important to understand that this information is not legal advice, but rather a general overview of foreclosure note fundamentals.

Holding a foreclosure note comes with specific risks, including uncertainty around the foreclosure timeline, exposure to legal expenses, and the potential for the property to be in poor condition due to neglect or vandalism. The likelihood of recovering the full value of a foreclosure note is influenced by the lien position—first liens generally have priority over junior liens—and by local property values. In Fort Collins, CO, strong property values may improve recovery prospects, but outcomes are still shaped by market conditions and the specifics of each note.

Non-Performing Notes in Fort Collins

Non-performing real estate notes are loans in which the borrower has fallen significantly behind on payments, typically by 90 days or more. For note holders in Fort Collins, CO, this situation often leads to an abrupt interruption of expected income, introducing considerable uncertainty regarding both the timing and likelihood of future payments. The unpredictability of cash flow can complicate financial planning and increase the risk profile of the investment.

When a note becomes non-performing, several resolution paths may be considered. These include negotiating a workout or loan modification with the borrower, or, if necessary, pursuing foreclosure as a last resort. Each approach carries its own risks and potential outcomes, and the optimal path often depends on the borrower’s circumstances and willingness to cooperate. Additionally, local market conditions in Fort Collins play a significant role in shaping exit strategies and influencing potential recovery values. Factors such as property demand, neighborhood trends, and regional economic health can all impact the time frame and financial results of resolving a non-performing note.

Bankruptcy Notes in Fort Collins

When a borrower files for bankruptcy, it initiates a legal process that can significantly impact the rights and timelines for private lenders and note holders. The moment bankruptcy is filed, an “automatic stay” goes into effect. This is a court order that temporarily halts most collection activities, including foreclosure proceedings, giving the borrower immediate relief from creditors while the bankruptcy case is reviewed.

There are two primary types of bankruptcy that affect mortgage debt: Chapter 7 and Chapter 13. Chapter 7, often called liquidation bankruptcy, may result in the sale of a borrower’s non-exempt assets to pay creditors, but does not provide a mechanism for catching up on missed mortgage payments. In contrast, Chapter 13 allows borrowers to propose a repayment plan, potentially enabling them to keep their property by making up overdue payments over time. For note holders in Fort Collins, CO, it’s important to understand that bankruptcy can delay or alter foreclosure timelines. In Colorado, the automatic stay pauses the foreclosure process, and any further action generally requires court approval. The duration and outcome depend on the type of bankruptcy filed and the borrower’s ability to meet court-approved obligations.

Senior Lien Holder Rights in Foreclosure in Fort Collins

Understanding lien priority is essential for note holders evaluating their position in Fort Collins, CO. Lien priority is determined by the order in which liens are recorded against a property, with the first recorded lien—often a mortgage or deed of trust—taking “first position.” Any subsequent liens, such as second mortgages or home equity lines of credit, are considered junior liens. This hierarchy directly impacts the rights and protections afforded to each lien holder.

At a foreclosure sale, the proceeds are distributed according to this established order. Senior lien holders are paid first, and only after their claims are fully satisfied do junior lien holders receive any remaining funds. This payout structure means that first position lien holders face less risk of loss, while junior lien holders are exposed to greater risk, especially if the property’s value does not cover all outstanding debts. In Fort Collins, where property equity levels can fluctuate, senior lien holders benefit from greater control over the foreclosure process, including the right to initiate proceedings and dictate terms. This control further secures their ability to recover owed amounts, making lien priority a critical factor in risk assessment for note holders.

City Violations and Note Risk in Fort Collins

Municipal or city code violations occur when a property fails to meet local regulations set by city authorities. These violations can include issues such as unsafe building structures, neglected yard maintenance, or the accumulation of unpaid fines from repeated citations. In Fort Collins, CO, code enforcement officers routinely inspect properties and issue notices when standards are not met, aiming to maintain neighborhood safety and community appearance.

When a property serving as collateral for a real estate note has unresolved code violations, its value and marketability can be significantly affected. Prospective buyers may be deterred by the prospect of inheriting costly repairs or outstanding municipal fines. In some cases, municipal liens resulting from unpaid violations may be recorded against the property, and depending on Colorado law, these liens can sometimes take priority over other claims, potentially impacting a note holder’s security position.

The local enforcement climate in Fort Collins plays a crucial role in determining risk for note holders. Active and consistent code enforcement means that compliance issues are more likely to be identified and escalated, increasing the urgency for resolution. Understanding how these violations are handled locally helps note holders make informed decisions about their investment and potential exit strategies.

If your note or property is tied to markets outside Fort Collins, savvy investors often keep an eye on opportunities across the Denver metro area, including Aurora. With strong population growth and consistent real estate activity, Aurora remains an active market for buying and selling promissory notes and deeds of trust. Many experienced note holders choose to convert long-term payments into immediate capital when the timing is right. If your deal is connected to that area, visit our Sell Your Note in Aurora Colorado page to see how quickly you can turn your note into cash.

If your note or property is tied to markets outside Fort Collins, savvy investors often keep an eye on opportunities across the Denver metro area, including Arvada. With steady growth and an active real estate market, Arvada continues to attract buyers interested in promissory notes and deeds of trust. Experienced note holders know that selling a note at the right time can unlock immediate capital while reducing long-term exposure. If your deal is connected to that area, visit our Sell Your Note in Arvada Colorado page to see how quickly you can convert your note into cash.