Your borrower is behind on payments. Maybe one month. Maybe six. Maybe more.

And you are wondering how much longer you can keep waiting for a situation that is not getting better on its own.

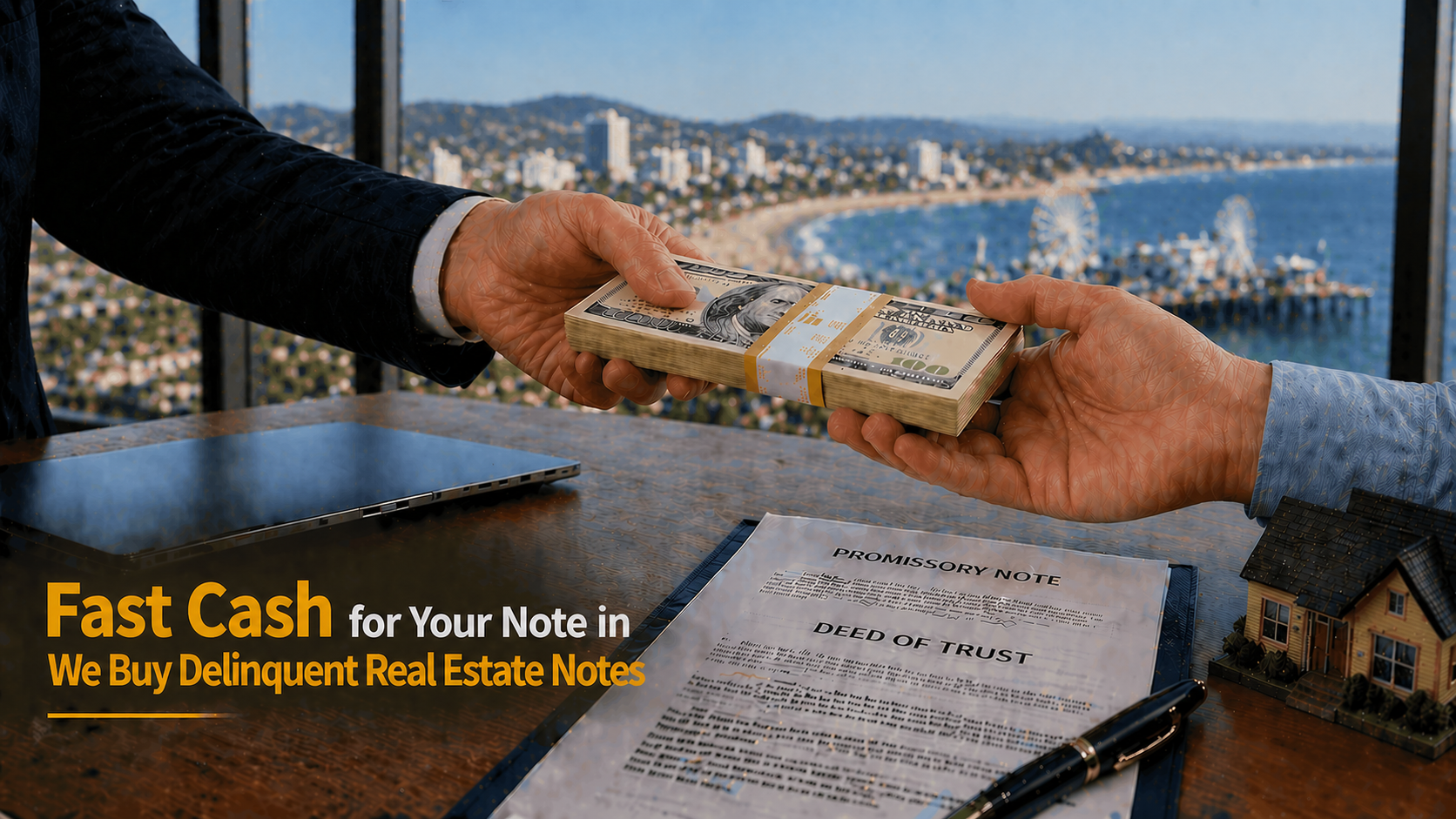

TrustedNoteBuyer.com buys delinquent real estate notes across all 50 states. We buy them at every stage of delinquency. We buy single notes and entire portfolios. And we pay cash — fast, fairly, and with zero fees.

You do not have to wait for the delinquency to turn into a full default. You do not have to fund a foreclosure to resolve it. And you do not have to keep managing a borrower who is not holding up their end of the agreement.

You can sell now. Get your cash. Move on.

What is a delinquent real estate note?

A real estate note becomes delinquent when the borrower misses one or more scheduled payments. Delinquency exists on a spectrum. A borrower who is 30 days late is technically delinquent. A borrower who is six months behind is seriously delinquent. And a borrower who is 90 or more days past due crosses the threshold that most note buyers define as non-performing.

Delinquency is not the same as default. Default typically occurs when the note holder issues a formal notice of default — a legal document that begins the foreclosure process. However, both situations create a market for your note. Furthermore, buyers like TrustedNoteBuyer.com purchase notes at every point on the delinquency spectrum — from the first missed payment through formal default and active foreclosure.

Your delinquent note still has real value

Many note holders assume that a delinquent note has lost its value. That assumption is wrong.

The value of a delinquent real estate note does not depend on the borrower’s payment behavior. It depends primarily on the real property securing the note. As long as there is equity in that property, there is real value in your note.

Furthermore, professional note buyers purchase delinquent notes because they have the tools and expertise to resolve them. They handle borrower negotiations, collection proceedings, and foreclosure actions every day. That expertise is what they are paying for when they acquire your note.

Therefore, a delinquent note is a distressed asset — not a worthless one. And it can be converted into guaranteed cash faster than most sellers expect.

We buy notes at every stage of delinquency

Some buyers only purchase notes that meet a specific delinquency threshold. We do not have that limitation.

One to two missed payments — early delinquency

A borrower who has missed one or two payments is in early-stage delinquency. The situation is concerning but not yet critical. There is still a reasonable chance the borrower will cure — either by catching up on payments, entering a repayment plan, or refinancing.

We purchase early-stage delinquent notes. The offer reflects the risk that the delinquency continues. However, a strong LTV and significant property equity often produce competitive offers even at this early stage. Furthermore, early-stage notes sometimes receive smaller discounts than deeply delinquent ones — because the probability of a cure is higher.

Three to six missed payments — moderate delinquency

A borrower three to six months behind is solidly non-performing. At 90 days past due, the note crosses the threshold most buyers define as non-performing. The probability of a voluntary cure decreases with each passing month.

At this stage, buyers evaluate the note increasingly based on the foreclosure outcome rather than the borrower’s likelihood of resuming payments. The LTV becomes even more important — because the collateral, rather than the borrower, is the primary source of recovery.

Six to twelve missed payments — serious delinquency

A borrower six to twelve months behind is seriously delinquent. The default is well established. Foreclosure is increasingly likely to be the resolution path. As a result, buyers price the note based primarily on the foreclosure timeline and the collateral value.

Despite the deeper discount at this stage, these notes are purchased regularly. A strong LTV — significant equity in the property — can still produce a competitive offer even after six to twelve months of missed payments.

More than twelve missed payments — severe delinquency

A borrower more than twelve months behind is severely delinquent. The note has likely been in formal default for some time. Foreclosure proceedings may have already started. The buyer is underwriting the full foreclosure outcome.

Even at this stage, the note has real value — as long as there is equity in the property. The offer reflects the deep discount required to account for the extended timeline, legal costs, and outcome uncertainty. However, selling at this stage is almost always better than continuing to wait.

Why the LTV matters more than the delinquency stage

Note holders often focus on the number of missed payments when thinking about their note’s value. However, the loan-to-value ratio is far more important.

Here is a clear example. Consider two notes — both with six months of missed payments.

Note A has a remaining balance of $130,000 on a property worth $240,000. The LTV is 54 percent. There is $110,000 of equity protecting the buyer’s investment. Despite six months of missed payments, this note will receive a strong offer.

Note B has a remaining balance of $195,000 on a property worth $210,000. The LTV is 93 percent. There is almost no equity. The buyer is taking on significant collateral risk. Consequently, this note receives a much deeper discount — not because of the missed payments but because of the thin equity position.

Therefore, know your LTV before you approach any buyer. It is the number that matters most — regardless of how many payments have been missed.

All types of delinquent real estate notes we buy

TrustedNoteBuyer.com purchases every type of delinquent real estate note. Your note type does not limit your options.

Residential mortgage notes

Single-family homes are the most common delinquent notes we purchase. They are the most straightforward to evaluate and produce the strongest offers. We also buy delinquent notes on two to four unit residential properties.

Commercial real estate notes

We purchase delinquent notes secured by office buildings, retail centers, industrial facilities, and mixed-use properties. Commercial notes are more complex. However, they are purchased regularly when the LTV is strong and the collateral has clear market value.

Owner financed and seller carryback notes

We buy delinquent owner financed notes and seller carryback notes regularly. These are among the most common private notes in the secondary market. Furthermore, documentation challenges are common with owner financed notes — and our team is experienced in resolving them efficiently.

Land contracts and contracts for deed

We purchase delinquent land contracts and contracts for deed secured by residential, commercial, and vacant land properties. Land contract delinquencies require specialized handling in many states. Our team understands those requirements thoroughly.

Trust deed notes

We buy delinquent notes secured by deeds of trust across all non-judicial foreclosure states. Trust deed delinquencies often move toward resolution faster than mortgage states — which typically produces stronger offers.

Note portfolios

We purchase delinquent note portfolios of all sizes — from two notes to hundreds. We buy mixed portfolios containing performing, delinquent, and non-performing notes together in a single transaction. Therefore, you do not need to sort your portfolio before approaching us.

Why selling is better than waiting for the borrower to cure

Many note holders hold on after payments start being missed — hoping the borrower will catch up. Sometimes that happens. However, waiting has real costs that compound every month.

Every missed payment is lost income

Each missed payment is money you were counting on. Furthermore, there is no guarantee those payments will ever be made up. Selling converts that lost income into a guaranteed lump sum — immediately.

Legal costs accumulate fast

Once delinquency progresses to formal default and foreclosure, legal costs begin accumulating rapidly. In slow judicial foreclosure states, those costs run for years. Selling now eliminates every future legal cost immediately.

Collateral value may be declining

A delinquent borrower often stops maintaining the property. Every month you wait, the property securing your note may be worth less. Therefore, selling sooner preserves more value than waiting.

The situation rarely improves on its own

Delinquent borrowers rarely self-correct without intervention. If they have missed several payments, they are typically facing a financial situation that will not resolve itself quickly. Waiting for a cure that may never come is not a strategy. Selling converts that uncertainty into guaranteed cash.

How to sell your delinquent real estate note — step by step

Step 1 — Gather your documents

Before reaching out, organize your core documents. Gather the original promissory note, the deed of trust or mortgage, a complete payment history showing every missed payment, any demand letters or default notices you have sent, and basic property information including a current value estimate.

The payment history is particularly important for delinquent notes. It shows exactly when payments stopped and how many have been missed. A well-documented payment history speeds up the evaluation and often produces a stronger offer.

Step 2 — Contact TrustedNoteBuyer.com

Reach out through our online form or speak directly with our team. Share the property address, unpaid principal balance, original loan terms, current delinquency status, and property type. Be transparent about the delinquency — including how many payments have been missed, whether a formal notice of default has been issued, and whether any foreclosure action has been filed.

Transparency upfront produces the most accurate offer and prevents delays during due diligence.

Step 3 — Receive your written cash offer

After reviewing your note and evaluating the collateral, we present a written cash offer within two to three business days. The offer reflects the delinquency stage, the LTV, the state’s foreclosure timeline, and the property type.

We explain every offer clearly. We walk you through the key factors that drove the number. There is no obligation to accept. There are no fees at any stage.

Step 4 — Accept and complete due diligence

Once you accept, due diligence begins immediately. We review your documents in detail. We confirm the loan terms, verify the collateral value, check the lien position, and identify any title issues. Due diligence typically takes one to two weeks with complete documentation.

Respond promptly to every request. The faster you respond, the faster you close.

Step 5 — Close and receive your funds

Closing is handled through a licensed title company or escrow agent. You sign the transfer documents. We fund the transaction. Your cash is wired directly to your bank account on closing day.

After closing, the note is ours. We take over the borrower relationship, all collection activity, and all legal proceedings. You walk away with cash and zero further obligations.

The entire process takes two to four weeks in most cases.

We buy delinquent note portfolios

Holding multiple delinquent real estate notes? Or a mixed portfolio of performing and delinquent notes?

You can sell everything in a single transaction.

TrustedNoteBuyer.com purchases delinquent note portfolios of all sizes. We buy two notes or two hundred notes in one closing. We handle performing and non-performing notes together. We buy notes at every stage of delinquency. And we work across all 50 states.

Portfolio sales close everything simultaneously. You deal with one buyer through one process. And you free up all of your capital at once.

Frequently asked questions

Can I sell a note after just one or two missed payments?

Yes. We purchase notes at every stage of delinquency — including notes with just one or two missed payments.

Will I get a better offer if I wait for more payments to be missed?

No — and often the opposite. Early-stage delinquent notes sometimes receive stronger offers because the probability of a cure is higher and the collateral may be in better condition. Waiting typically does not improve your offer. Furthermore, it often makes it worse.

What if the borrower has made some partial payments?

Partial payments affect how the note is classified and priced. Share all payment details — including partial payments — when you submit your note. Full transparency produces the most accurate offer.

Can I sell a delinquent note if I have already hired a foreclosure attorney?

Yes. Having a foreclosure attorney engaged does not prevent a sale. However, notify your attorney of the pending transaction so they can pause any legal proceedings during the sale process.

Does the reason for the missed payments affect my offer?

The reason for the delinquency is less important than the LTV and the property value. However, a borrower who missed payments due to a temporary hardship — and who has equity in the property — may be more likely to cure. Buyers factor that probability into their evaluation.

Does TrustedNoteBuyer.com buy delinquent notes in all 50 states?

Yes. We purchase delinquent real estate notes across all 50 states — single notes and portfolios, all property types, all stages of delinquency.

The bottom line

TrustedNoteBuyer.com buys delinquent real estate notes across all 50 states. All note types. All delinquency stages. Single notes and portfolios of any size.

No fees. No brokers. No obligation. Fast offers and faster closings.

Ready to sell your delinquent real estate note? Get your free offer at TrustedNoteBuyer.com today.

Investors buying non performing notes seek opportunities in distressed assets with potential upside. They understand the risks and structure offers accordingly. Selling to these investors provides a fast and effective way to liquidate.

Note buyers for distressed assets focus on acquiring underperforming or troubled notes. These assets often involve missed payments or legal complications. A direct sale to these buyers provides a clean and efficient exit.

We buy bad mortgage notes tied to unreliable borrowers or inconsistent payment histories. These notes can negatively impact your portfolio over time. Selling to a direct buyer provides a clean exit and immediate liquidity.