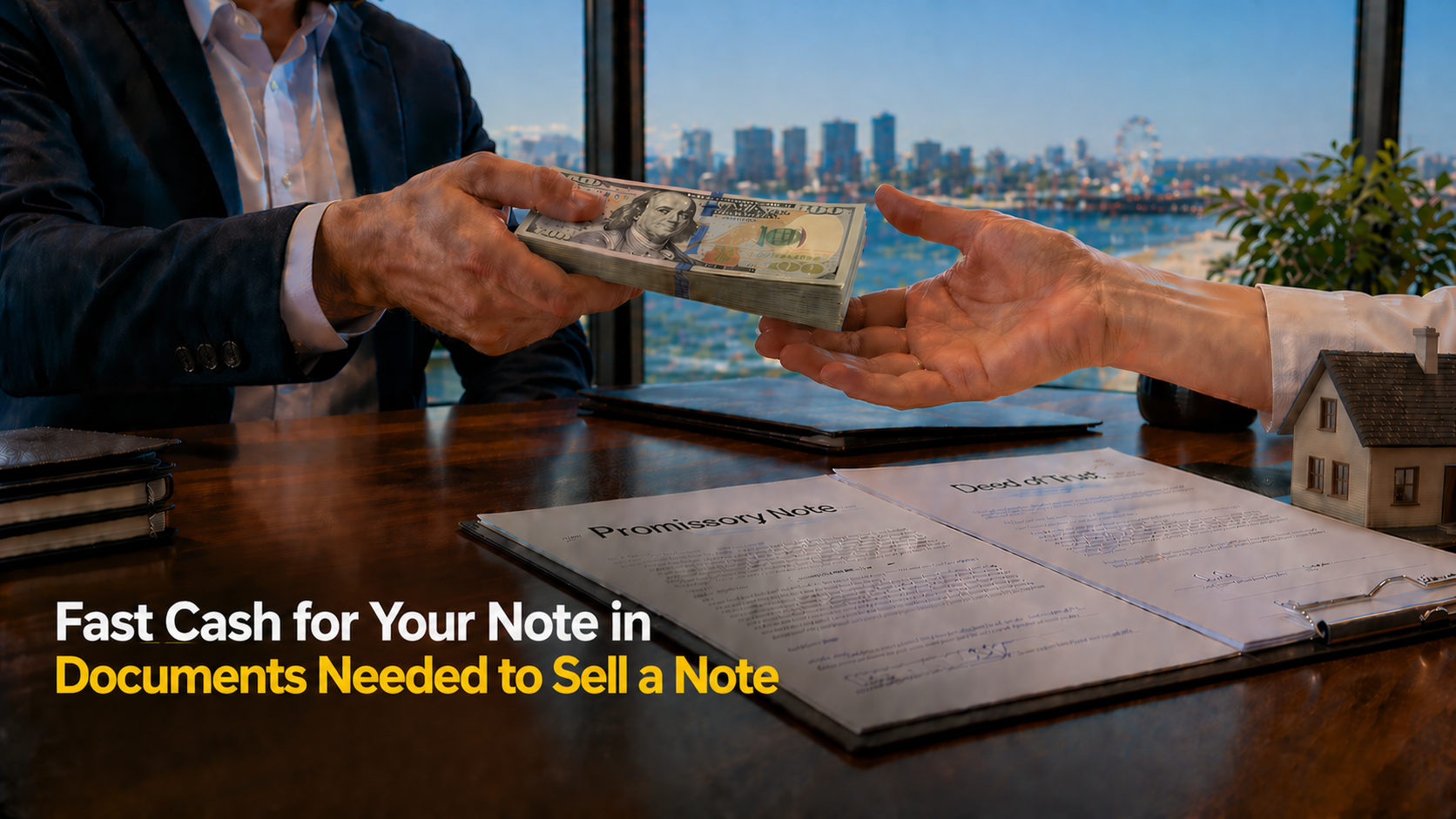

You are ready to sell your real estate note. You have found a buyer. And now they are asking for documents.

What exactly do you need? How do you find everything? And what happens if something is missing?

This article answers all of those questions clearly and completely. Having the right documents ready before you reach out to a buyer speeds up the process, strengthens your offer, and gets you to closing faster.

Why documentation matters so much in a note sale

Documents are not just paperwork. They are the foundation of the entire transaction.

A note buyer cannot evaluate your note without them. They cannot confirm the loan terms, verify the collateral, or check the lien position without reviewing the original documents. Furthermore, incomplete documentation introduces uncertainty — and uncertainty always reduces the offer you receive.

Organized sellers close faster. They receive stronger offers. And they encounter fewer surprises during due diligence. Therefore, gathering your documents before you reach out to a buyer is always worth the effort.

The core documents every note sale requires

These are the essential documents that every note buyer needs — regardless of whether your note is performing or non-performing.

1. The original promissory note

This is the single most important document in any note transaction. It is the legal record of the borrower’s promise to repay the loan. It outlines every original loan term — the principal balance, the interest rate, the payment schedule, and the maturity date.

Without the original promissory note, no buyer can evaluate or close on your note. Therefore, finding this document is your first priority.

If you cannot locate the original, do not panic. There are options. A copy may be held by the title company that handled the original closing. It may also be on file with the county recorder’s office or with your original escrow agent. Additionally, a note reconstruction attorney can sometimes help recreate a lost note — though this adds time and cost to the process.

2. The deed of trust or mortgage

This document secures the note against the real property. It gives the note holder the legal right to foreclose if the borrower defaults. It also confirms the lien position — first, second, or junior.

Lien position matters enormously. First lien notes have the highest priority claim on the property in a foreclosure. They are the most valuable and receive the strongest offers. Second and junior lien notes carry more risk because they are paid only after the first lien holder is satisfied.

Make sure you know your lien position before approaching any buyer. Furthermore, confirm that the deed of trust or mortgage was properly recorded with the county recorder’s office at the time of origination.

3. The note endorsement or allonge

If the note has been transferred or sold previously, you will need documentation of that transfer. An endorsement is a signature on the back of the original note transferring ownership. An allonge is a separate document attached to the note that records the transfer when there is no room on the original.

If you purchased the note from someone else, make sure you have a complete chain of endorsements from the original lender to you. Gaps in the chain of title can delay or derail a transaction. Therefore, review this carefully before reaching out to a buyer.

4. A complete payment history

The payment history is a record of every payment made — and every payment missed — from the origination of the note to the present day. It shows the buyer exactly how the borrower has performed over the life of the loan.

For performing notes, a clean payment history confirms the note is in good standing and supports a stronger offer. For non-performing notes, the payment history shows when payments stopped and how long the borrower has been in default. Additionally, a history of consistent payments before the default began signals that the borrower had — and may still have — the capacity to pay.

Pull this record from your files, your loan servicer, or your bank statements. The more complete and organized it is, the better.

5. The title insurance policy

A title insurance policy was typically issued at the time the original loan was made. It protects the lender against title defects, liens, and other issues that could affect ownership of the property.

Including a copy of the title policy speeds up due diligence significantly. It gives the buyer confidence that the title was clean at origination and helps identify any issues that may have arisen since. Therefore, locate this document and include it in your file from the start.

Additional documents for non-performing notes

If your note is non-performing — meaning the borrower is behind on payments, in default, or in foreclosure — you will need additional documents beyond the core set.

Notice of default

A notice of default is a formal legal document recorded with the county that signals the beginning of the foreclosure process. If one has been filed on your note, obtain a copy. It confirms the default is on the public record and gives buyers clarity about the legal status of the situation.

Lis pendens or foreclosure petition

If a foreclosure action has been filed in court, obtain a copy of the lis pendens or foreclosure petition. This document confirms that legal proceedings are officially underway. Furthermore, it tells the buyer what stage the foreclosure process is in and what steps remain before resolution.

Foreclosure sale date notice

If a foreclosure sale date has been scheduled, provide documentation confirming the date and details. Being close to a sale date can actually work in your favor — it signals that the resolution is imminent and reduces the buyer’s timeline uncertainty.

Borrower correspondence

Any written communication between you and the borrower regarding the default is valuable. This includes demand letters, notices of default, loan modification requests, and any responses from the borrower. This correspondence helps the buyer understand the borrower’s attitude toward the situation — whether they are cooperative, unresponsive, or actively contesting the default.

Bankruptcy filings

If the borrower has filed for bankruptcy, provide a copy of the bankruptcy petition and any relevant court orders. Bankruptcy does not prevent a note sale. However, it does affect the resolution process and the buyer needs to know about it upfront. Failing to disclose a bankruptcy can delay or kill a transaction entirely.

Property-related documents

The property securing your note is the buyer’s primary protection. Therefore, property-related documents play an important role in the evaluation process.

Property appraisal or broker price opinion

A recent appraisal or broker price opinion — commonly called a BPO — gives the buyer confidence in the current market value of the collateral. It helps confirm the loan-to-value ratio quickly and accurately. If you have a recent appraisal, include it. If you do not, the buyer will typically order their own during due diligence.

Property tax records

Current property tax records confirm that taxes are paid and up to date. Unpaid property taxes create a senior lien on the property that can take priority over your note in a foreclosure. Therefore, confirming tax status early prevents surprises during due diligence.

HOA documents

If the property is subject to a homeowners association, obtain current HOA records. Unpaid HOA assessments can create additional liens on the property. Furthermore, HOA rules and restrictions can affect the buyer’s plans for the property after resolution.

Property photos or inspection report

Current photos of the property help the buyer assess its condition quickly. A formal inspection report is even better. Good condition supports the collateral value and can strengthen your offer. Poor condition is better disclosed upfront than discovered during due diligence — surprises at that stage can reduce offers or delay closings.

Documents needed for portfolio note sales

If you are selling a portfolio of notes — multiple notes in a single transaction — you will need everything listed above for each individual note. Additionally, you will need a note tape.

The note tape

A note tape is a spreadsheet summarizing the key details of every note in the portfolio. It typically includes the property address, unpaid principal balance, interest rate, payment status, lien position, property type, and default status for each note.

The note tape is the first thing a portfolio buyer reviews. It gives them an at-a-glance picture of the entire portfolio before they dive into individual file reviews. Therefore, preparing a clean, accurate note tape is essential for any portfolio sale.

Organize the note tape clearly. Use consistent formatting. Include all relevant details for every note. A well-prepared note tape signals that you are a serious, organized seller — and that tends to produce stronger offers.

What if documents are missing?

Missing documents are common — especially on older notes or notes that have been transferred multiple times. The good news is that missing documents are rarely a dealbreaker.

Here is what to do if something is missing.

The original promissory note is the most critical. If it is lost, check with the title company from the original closing, the county recorder’s office, and your original escrow agent. A note reconstruction attorney can sometimes help if the note cannot be located.

A missing deed of trust or mortgage can usually be obtained from the county recorder’s office, where it was recorded at origination. Most counties now have online search portals that make this straightforward.

Payment history gaps can sometimes be reconstructed from bank statements, deposit records, or servicer records. Partial records are better than none. Therefore, provide whatever you have and explain the gaps clearly.

A reputable note buyer works with you to resolve documentation gaps. They do not walk away at the first missing document. However, the more complete your file, the faster and smoother the process will be.

How to organize your documents for submission

Presentation matters. A well-organized submission file signals professionalism and builds buyer confidence. Here is a simple way to organize your documents before submitting.

Create a single folder — digital or physical — for each note. Label it clearly with the property address and borrower name. Organize the documents in this order: promissory note, deed of trust or mortgage, endorsements or allonge, payment history, title policy, default and foreclosure documents, property information, and any borrower correspondence.

For portfolio sales, create individual folders for each note and one master folder containing the note tape and any portfolio-level documents.

Scan everything to PDF if you are submitting digitally. Make sure scans are clear and legible. Blurry or incomplete scans slow down the review process.

Frequently asked questions

What is the most important document in a note sale?

The original promissory note is the most critical document. Without it, no buyer can evaluate or close on your note. Locating it is always the first priority.

Can I sell my note if I am missing documents?

In many cases, yes. Missing documents can often be replaced or reconstructed. Contact TrustedNoteBuyer.com to discuss your specific situation. We work with sellers to resolve documentation gaps regularly.

Do I need a title search before selling?

You do not need to order a title search yourself. However, providing an existing title policy speeds up due diligence. The buyer will typically order their own title search as part of the due diligence process.

What is a note tape and do I need one?

A note tape is a spreadsheet summarizing key details for each note in a portfolio. It is essential for portfolio sales. For single note sales, it is not required — but providing a clear summary of your note’s key details helps the process move faster.

Does TrustedNoteBuyer.com help with missing documents?

Yes. We work with sellers regularly to help locate or reconstruct missing documents. Incomplete documentation slows things down but rarely prevents a transaction from closing.

How should I submit my documents?

You can submit documents digitally through our online form at TrustedNoteBuyer.com or by working directly with our team. Clear PDF scans of all documents are preferred.

The bottom line

Having the right documents ready before you approach a buyer is the single most impactful thing you can do to speed up your note sale and strengthen your offer.

The core documents are the promissory note, deed of trust or mortgage, endorsements, payment history, and title policy. Non-performing notes require additional default and foreclosure documentation. Portfolio sales require a clean note tape for every note in the portfolio.

TrustedNoteBuyer.com buys real estate notes across all 50 states — performing, non-performing, single notes, and portfolios. No fees. No brokers. No obligation.

Ready to get started? Submit your documents and get your free offer at TrustedNoteBuyer.com today.

Cashing out a non performing note gives you immediate access to capital instead of waiting on uncertain payments. This approach allows you to eliminate risk and improve liquidity. A direct buyer simplifies the process and provides a fast, structured payout.

Converting a non performing note to cash is one of the most effective ways to regain financial control. Rather than managing a problem asset, you can secure a lump sum and move forward. The process is straightforward when working with an experienced buyer.

Second position non performing notes carry added risk because recovery depends on the first lien position. These assets can be uncertain and difficult to resolve. Selling the note allows you to reduce exposure and recover value quickly.